Airdrop

Share

An Airdrop is a distribution of free tokens to a community, typically used as a marketing tool or a reward for early protocol adopters and testers. In 2026, the "points-to-airdrop" model has matured into merit-based incentive programs that utilize Sybil-resistance and Proof-of-Humanity to filter out bots. Airdrops remain a primary method for decentralized governance (DAO) bootstrapping. Follow this tag for the latest on retroactive rewards, eligibility criteria, and how to participate in the most anticipated token distributions in the ecosystem.

5443 Articles

Created: 2026/02/02 18:52

Updated: 2026/02/02 18:52

Recommended by active authors

Latest Articles

Was Kyle Samani’s Exit Coincidental?

2026/02/09 04:22

Trump raked over the coals for ‘embarrassing’ meltdown about American Olympic skier

2026/02/09 04:07

The Insiders Know Something: 200 Consecutive Sales as Markets Crumble

2026/02/09 04:03

Rap Star Drake Uses Stake to Wager $1M in Bitcoin on Patriots Despite Super Bowl LX Odds

2026/02/09 04:00

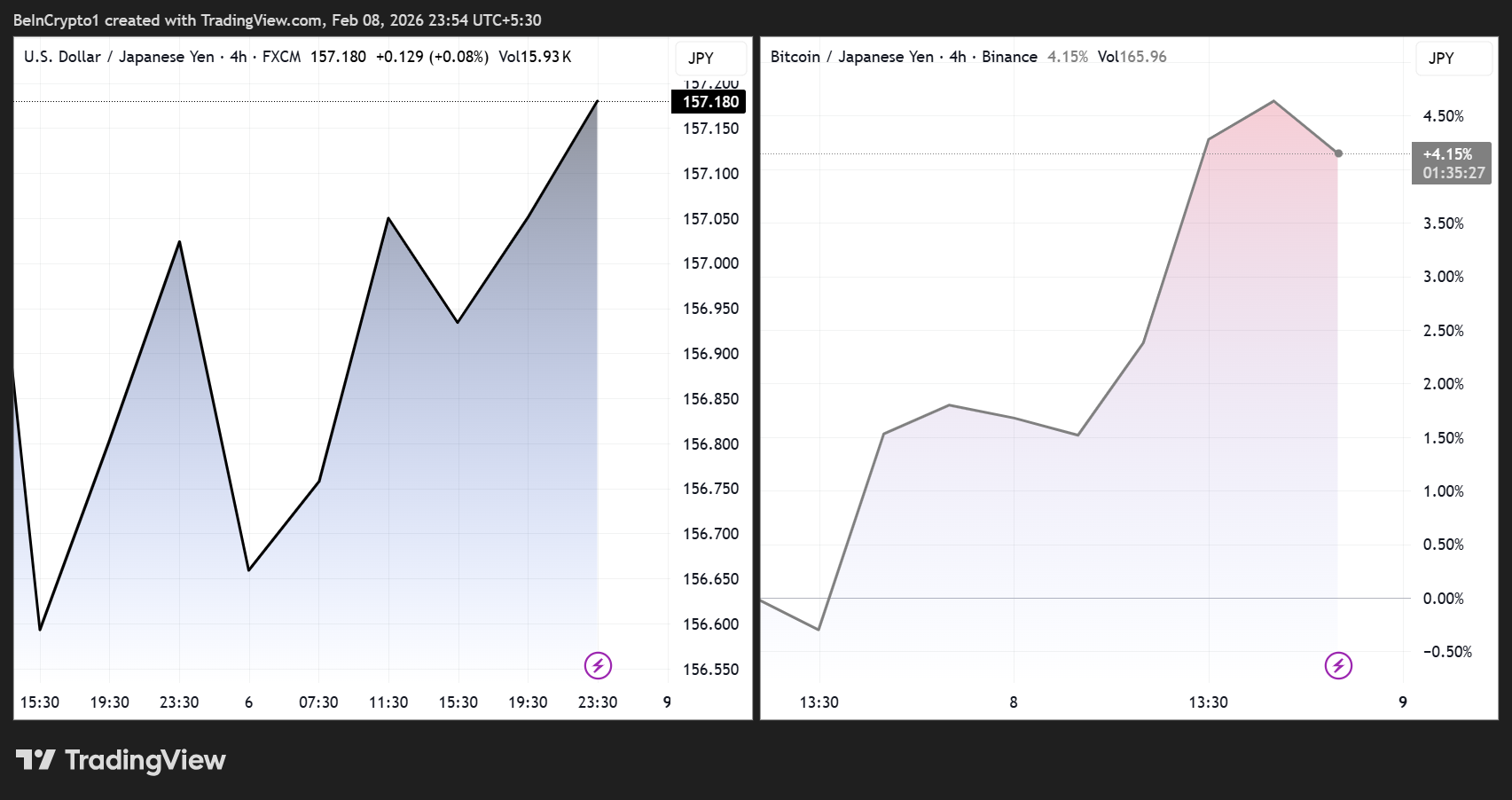

Markets and Crypto Eye Policy Reforms As Japan’s Sanae Takaichi Secures Historic Victory

2026/02/09 03:31