Tesla’s 13% Rally Sets Up a Balanced Risk Reward Ahead of Q2 Delivery Numbers

The post Tesla’s 13% Rally Sets Up a Balanced Risk Reward Ahead of Q2 Delivery Numbers appeared first on 24/7 Wall St..

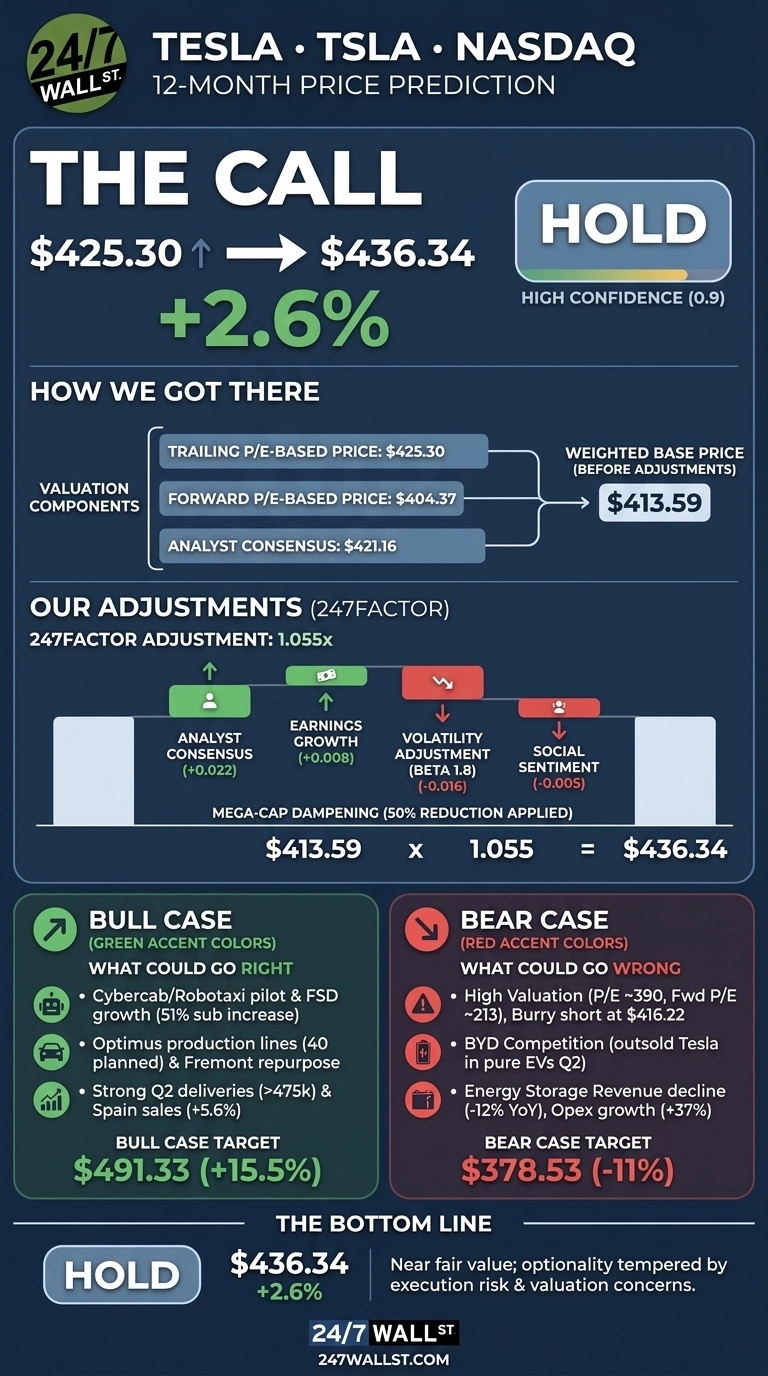

Tesla (NASDAQ:TSLA) shares have staged a sharp rebound heading into the Q2 delivery release, and my proprietary model now pegs the stock right on top of fair value. Tesla closed at $425.30 on July 1, 2026, after a 13.25% rally over the past week.

My 24/7 Wall St. price target for Tesla is $436.34, implying 2.6% upside over the next 12 months. That is a hold, and my confidence is high.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $425.30 |

| 24/7 Wall St. Price Target | $436.34 |

| Upside | 2.6% |

| Recommendation | HOLD |

| Confidence Level | 90% |

A Rebound Into a Soft Delivery Report

Tesla is down 5.43% year to date but up 41.43% over the past year, and shares sit 16% below the 52-week high of $498.83.

Bloomberg estimated Q2 deliveries at 396,466 units, up roughly 3% year over year, while BYD delivered 557,090 battery EVs in the same window. Regional data is bifurcated: Spain sales climbed 5.6% in June while Norway registrations fell 43%. Q1 was the offset, with revenue of $22.39 billion, non-GAAP EPS of $0.41, and automotive gross margin expanding to 21.1% from 16.2%.

24/7 Wall St.

24/7 Wall St.

Why Bulls See a Breakout Ahead

The bull thesis rests on optionality that traditional multiples cannot capture. Cybercab entered pilot production at Gigafactory Texas, unsupervised Robotaxi rides launched in Dallas and Houston in April, and FSD active subscriptions grew 51% to 1.28 million.

Elon Musk this week confirmed the Fremont Model S/X line is being repurposed for Optimus, with 40 production lines planned targeting one million robots.

My bull-case scenario points to $491.33 in 12 months, a 15.53% return, and Polymarket traders assign an 83.5% probability that TSLA touches $435 in July.

The Risks Worth Watching

Valuation is the tightest constraint. The trailing P/E of 390 and forward P/E of 213 leave little margin for delivery disappointment, and Michael Burry disclosed a fresh short at $416.22. Energy storage revenue fell 12% year over year in Q1, opex grew 37%, and BYD is now out-shipping Tesla in pure EVs.

Bulls would counter that the opex surge reflects AI R&D and the CEO comp award, both of which should convert to Optimus and Robotaxi revenue in later years. My bear-case scenario sits at $378.53, or a -11% return.

Hold Into Deliveries, Reassess After

My 24/7 Wall St. price target of $436.34 reflects a stock that has already run into fair value on automotive fundamentals, with AI and robotics optionality tempered by execution risk and multiple compression. Confidence is high at 90%.

I would get more constructive if Q2 deliveries surprise above the Polymarket 475,000 threshold or Optimus hits a firm production milestone. I would stay cautious if regulatory credits keep sliding and Robotaxi expansion slips past 1H 2026.

Looking further ahead, here is where our model projects Tesla could trade, extending the base-case trajectory from our five-year scenario.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $436 |

| 2027 | $455 |

| 2028 | $475 |

| 2029 | $495 |

| 2030 | $515 |

These projections assume Tesla executes on Cybercab, Optimus, and FSD monetization while defending automotive margin. Meaningful upside or downside could result from Robotaxi network economics, China FSD approval, or a sharper EV price war with BYD.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and Tesla didn’t make the cut. Grab the names FREE today.

The post Tesla’s 13% Rally Sets Up a Balanced Risk Reward Ahead of Q2 Delivery Numbers appeared first on 24/7 Wall St..

Ayrıca Şunları da Beğenebilirsiniz

AI predicts XRP price for April 30, 2026

Cryptopolitan Launches Crypto Data Dashboards and Becomes the First Media Platform with Full Agentic AI Access