Broadcom Near a Reset Multiple. Here’s Where the Stock Could Go in 2026

Key Stats for Broadcom Stock

- Current Price: $365.02

- Target Price (Mid): ~$1,010

- Street Target: ~$525

- Potential Total Return: ~177%

- Annualized IRR: ~26% / year

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Broadcom (AVGO) helped the most-watched company in artificial intelligence unveil its first custom chip, and the market barely flinched. On June 24, OpenAI and Broadcom unveiled Jalapeño, OpenAI’s first custom inference chip, an application-specific accelerator built only to run large language models rather than train them. OpenAI designed it; Broadcom handled the silicon implementation and manufacturing. The stock dipped roughly 3% that day on broad semiconductor weakness, not on the news itself. That muted reaction is the tension worth sitting with. A reveal that would have moved AVGO sharply a year ago now lands into a stock that fell 12.59% on June 4 after a record quarter, and the market cannot decide whether Broadcom is still a momentum trade or has quietly become a value one.

The case for the second reading starts with what the chip represents for Broadcom specifically. OpenAI now joins Google, Meta, Anthropic, and two undisclosed names as the sixth core customer in Broadcom’s custom-silicon roster. That breadth is the heart of the bull thesis, because it means Broadcom’s AI revenue no longer rests on any single hyperscaler’s spending decisions. The reveal itself confirms a pattern: every frontier lab now wants custom silicon to escape GPU pricing, and Broadcom is the design partner of choice for that shift.

A Record Quarter the Market Punished Anyway

To understand why a strong reveal produced a shrug, you have to go back three weeks. Broadcom reported fiscal Q2 revenue of $22.19 billion on June 3, up 48% year over year, with AI semiconductor revenue of $10.8 billion growing 143%. Free cash flow hit a record $10.3 billion. By any plain reading, the quarter was excellent. The stock fell 12.59% the following day anyway, the steepest of its last five earnings reactions.

The reason was guidance, not results. Q3 AI revenue was guided to $16 billion, below the most aggressive Street estimates near $17.2 billion, and CEO Hock Tan reaffirmed rather than raised the $100 billion-plus AI target for fiscal 2027. When a stock is priced for perfection, holding steady reads as a miss. That dynamic, where the business grows fast, and the stock still gets hit because expectations grew faster, is the central problem facing every AI name right now.

What the selloff did, though, was reset the multiple. AVGO now trades at an NTM EV/EBITDA (enterprise value to forward earnings before interest, taxes, depreciation, and amortization) of 18.68x. A quarter ago, that figure was 24.83x, and two quarters ago it was 25.25x. The fundamentals improved while the multiple the market is willing to pay contracted hard. That is the gap the model is built to interrogate.

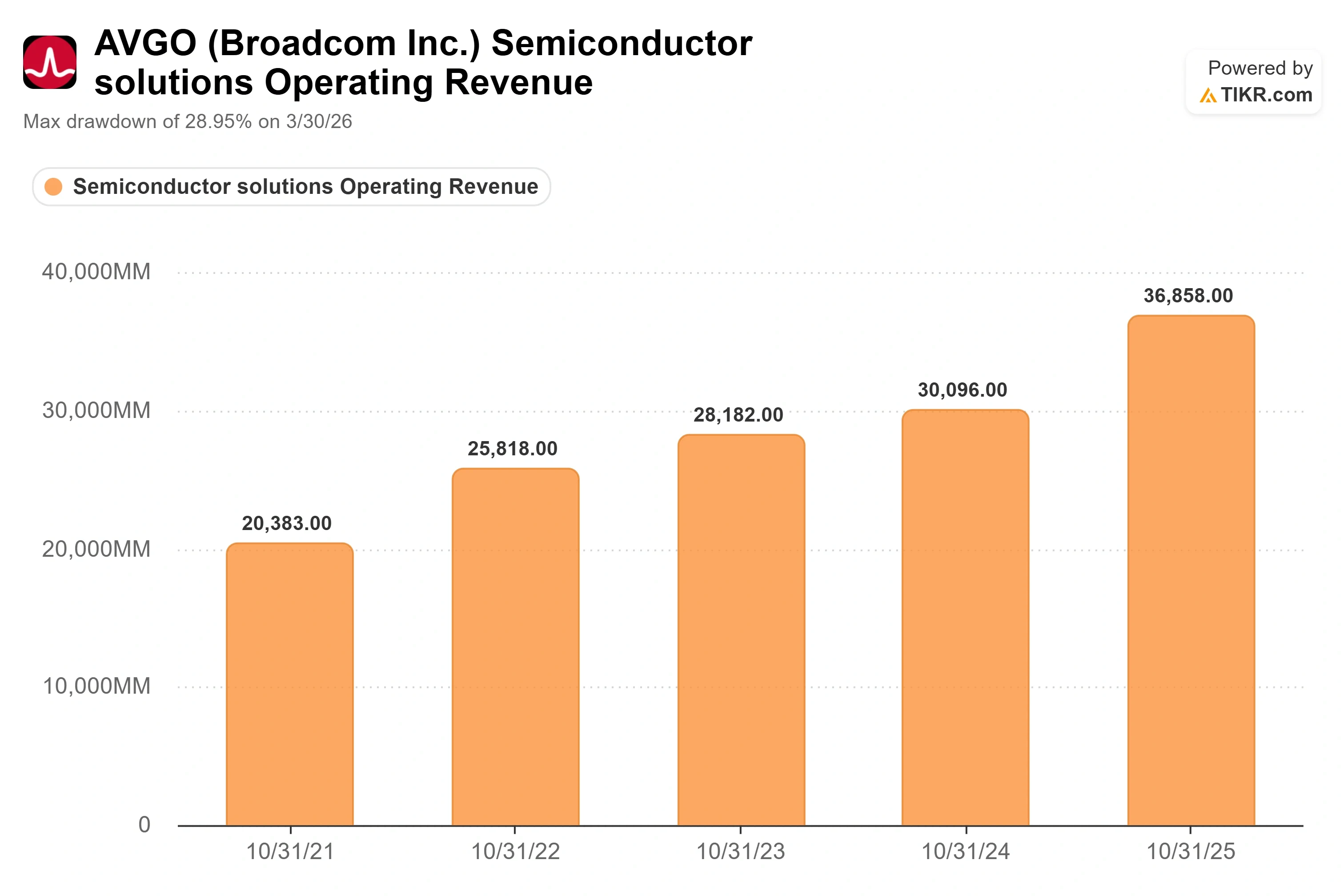

Broadcom Semiconductor Operating Revenue (TIKR)

Broadcom Semiconductor Operating Revenue (TIKR)

See historical and forward estimates for Broadcom stock (It’s free!) >>>

What Jalapeño Confirms About the Thesis

Tan did not mince words on the Q2 call about where demand sits. “Bookings for AI semiconductors were over $30 billion against the $10.8 billion we shipped,” he said. That ratio, nearly three dollars booked for every dollar delivered, is the single most important number in the quarter, because it tells you the order book is filling faster than the company can ship. Tan described the demand as “simply insatiable” and said visibility now runs through 2028.

Jalapeño is the proof point. Broadcom CEO Hock Tan told Bloomberg the chip delivers roughly 50% lower inference cost per token than current-generation GPUs. That figure is Tan’s own, from early lab testing, and is not yet independently benchmarked. OpenAI’s own statement was more measured, describing performance per watt as “substantially better than current state-of-the-art,” with a full technical report promised in the coming months. Treat the 50% number with caution. What matters for Broadcom either way is structural: the chip ships to OpenAI, but the strategic win is that Broadcom’s addressable demand keeps widening as more labs design their own silicon.

The competitive picture supports a premium, though a smaller one than before. Against semiconductor peers on the TIKR Competitors page, AVGO trades at an NTM P/E of 23.18x, below the peer mean of 40.06x and the median of 35.87x. NVIDIA sits at 19.37x and SK Hynix at 7.25x, while Marvell trades at 58.81x and AMD at 59.82x. Broadcom is not the cheapest AI chip name, but it is priced well below the group average despite carrying some of the most durable multi-year contracts in the sector. That discount to peers reads more like a post-earnings reset that has not fully recovered than a structural penalty.

Broadcom NTM EV/EBITDA (TIKR)

Broadcom NTM EV/EBITDA (TIKR)

See how Broadcom performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $365.02

- Target Price (Mid): ~$1,010

- Potential Total Return: ~177%

- Annualized IRR: ~26% / year

Broadcom Advanced Valuation Model (TIKR)

Broadcom Advanced Valuation Model (TIKR)

See analysts’ growth forecasts and price targets for Broadcom stock (It’s free!) >>>

TIKR’s mid-case model values AVGO at around $1,010 by October 2030, implying roughly 177% total return from the current price, or about 26% annualized over the next 4.3 years. The two revenue drivers behind that target are AI semiconductor scaling, where management guides revenue to double in the second half of fiscal 2026 and exceed $100 billion in fiscal 2027, and the VMware software base, where annual recurring revenue grew 17% year over year. The margin driver is mix and operating leverage: software gross margins above 93% offset lower custom-silicon margins, and management expects operating margin to hold near 67% even as AI revenue grows as a share of the total. The model assumes net income margins expanding toward around 55% over the forecast.

The primary risk is customer concentration. A meaningful share of AI revenue traces to a handful of hyperscalers, and a shift in any one customer’s chip strategy would hit the model directly. The upside is that the six-customer roster, now anchored by the OpenAI reveal, broadens that base faster than bears expected. The downside is that the multiple compresses further if AI order growth decelerates, which would pull the realized return below the model’s mid case even if revenue holds.

Conclusion

The number that settles this debate arrives around early September, when Broadcom reports fiscal Q3. The guide is $16 billion in AI revenue at over 200% year-over-year growth. Hit or beat it, and the June selloff looks like the reset that handed long-term buyers a better entry into one of the most contracted AI businesses in the market. Miss it by even a modest margin at this still-premium multiple, and the reaction will be sharper than June’s was, because the company set the bar itself. Watch the AI revenue line first, then watch whether management’s commentary on capital returns shifts, since a step-up in buybacks would signal confidence that the order book converts on schedule.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Broadcom?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Broadcom, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Broadcom alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Broadcom on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!

You May Also Like

On-Chain Data Tracks Machi Big Brother ETH Leverage Defense on Hyperliquid

'Not the picture to show': MAGA movie star mocked over revealing pic making Trump look bad

Crypto Stocks Lag Behind as Market Divergence Widens