Only 46% of Americans Have a Three-Month Emergency Fund. The Trend Is Getting Worse.

The post Only 46% of Americans Have a Three-Month Emergency Fund. The Trend Is Getting Worse. appeared first on 24/7 Wall St..

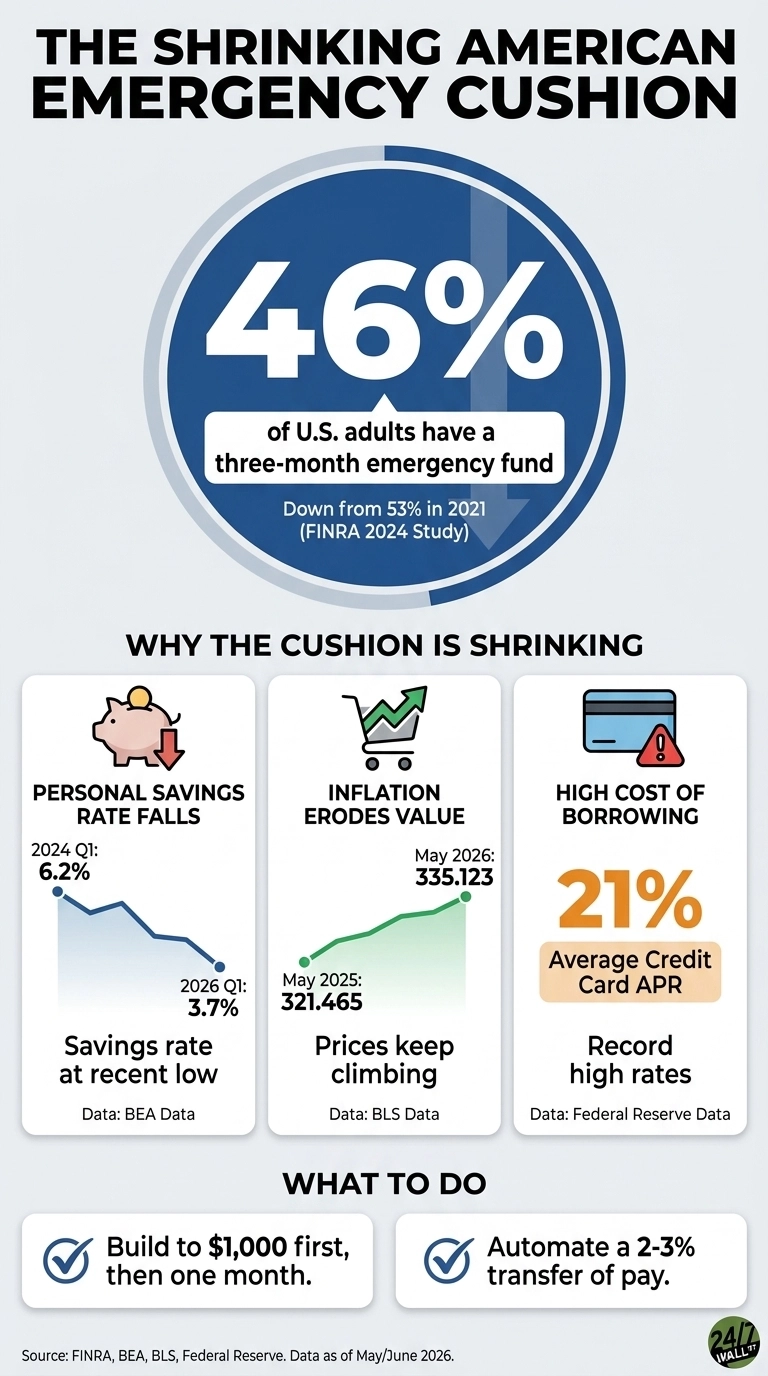

- Only 46% of Americans have three months of emergency savings, down from 53% in 2021, erasing over a decade of progress.

- The personal savings rate collapsed to 3.7% in early 2026 from 6.2% two years earlier as Americans spend 92.6% of disposable income.

- Low-income households earning under $25,000 are 3 times less likely to have emergency funds than those earning over $75,000.

- Credit card debt now carries a record 21% average APR, making unexpected expenses a gateway to expensive debt for struggling households.

- 26% of Americans spent more than their income in 2024, the highest rate in FINRA's study history, up from 19% in 2021.

- Are you ahead, or behind on retirement? SmartAsset's free tool can match you with a financial advisor in minutes to help you answer that today. Each advisor has been carefully vetted, and must act in your best interests. Don't waste another minute; learn more here.

The headline number that gets thrown around in personal finance, that most Americans cannot cover a $1,000 emergency, sounds like clickbait until you look at what the surveys actually show. The reality may be worse. According to the FINRA Foundation’s 2024 National Financial Capability Study, only 46% of U.S. adults have set aside enough money to cover three months of living expenses in an emergency. That leaves a majority without a meaningful buffer, and the trend has recently moved in the wrong direction.

The number is moving in the wrong direction

The 46% figure marks a notable drop from 53% in 2021, reversing gains that had built steadily from 2009 through the pandemic. For context, in 2009, only 36% of Americans had three months of emergency savings. It took more than a decade to push that number higher, and a meaningful portion of that progress has been erased in just a few years.

24/7 Wall St.This infographic shows that only 46% of U.S. adults have a three-month emergency fund, down from 53% in 2021. This decline is attributed to factors such as falling personal savings rates, inflation eroding value, and high borrowing costs, with actionable steps provided to build savings.

24/7 Wall St.This infographic shows that only 46% of U.S. adults have a three-month emergency fund, down from 53% in 2021. This decline is attributed to factors such as falling personal savings rates, inflation eroding value, and high borrowing costs, with actionable steps provided to build savings.

The savings slowdown is also visible in broader economic data, though the exact figures move over time. The personal savings rate has declined sharply from pandemic-era highs and remains low by historical standards. Americans are spending a larger share of their income, leaving less available for unexpected expenses.

Who actually has a cushion, and who doesn’t

The national average hides a much harsher picture once you slice the FINRA data by income, age, and education. The gap between the people who can absorb a shock and the people who cannot is enormous:

- By income: 22% of households earning under $25,000 have three months of rainy day funds, compared with 66% of households earning above $75,000.

- By age: 36% of adults ages 18 to 34 have an emergency fund, versus 59% of adults 55 and older.

- By education: 33% of those with a high school degree or less, versus 64% of college graduates.

The income gap is the one that matters most for the $1,000 question. Higher earners are roughly three times as likely to have an emergency fund as lower earners, which means a flat tire or an ER copay is a budgeting inconvenience for one household and a debt event for another.

Why the cushion is shrinking

The squeeze is coming from several directions at once. Prices have continued to rise over the past year, while real wage growth has been uneven, meaning paychecks are not stretching as far after inflation. At the same time, the fallback option when savings fall short, credit cards, now carry average interest rates around 21%, near record highs. That combination makes it harder to build savings and more expensive to operate without them.

FINRA’s data clearly captures that pressure, and the share of adults who report spending more than their income rose to 26% in 2024, up from 19% in 2021. Meanwhile, average annual household spending reached $78,535 in 2024, according to the BLS Consumer Expenditure Survey. Consumer sentiment has also remained weak, with the University of Michigan index sitting well below long-term averages in 2026, reflecting a broadly cautious outlook.

What this means for your own number

The takeaway: the $1,000 emergency benchmark is a floor, not a goal. If a four-figure car repair would force you to carry a balance at 21% APR, you are in the majority, and the majority is in a worse position than it was three years ago. Two practical moves the data supports:

- Build to $1,000 first, then to one month of expenses. The FINRA gap between people who have three months saved and people who don’t tracks closely with income, but the first $1,000 is where the swing from “borrow at 21%” to “pay cash” actually happens.

- Automate before you optimize. The decline in the savings rate in recent years reflects, in part, how little income is being consistently set aside. Setting up an automatic transfer, even 2% to 3% of each paycheck, rebuilds a buffer without relying on month-to-month decisions.

The data does not yet point to a clear turnaround. Prices have risen, borrowing costs remain high, and the savings rate is still low relative to historical norms. The result is a tougher environment for building an emergency cushion at a time when more households need one.

If You’ve Been Thinking About Retirement, Pay Attention (sponsor)

Retirement planning doesn’t have to feel overwhelming. The key is finding expert guidance, and SmartAsset’s simple quiz makes it easier than ever for you to connect with a vetted financial advisor. Here’s how:

-

Answer a Few Simple Questions.

-

Get Matched with Vetted Advisors

-

Choose Your Fit

Why wait? Start building the retirement you’ve always dreamed of. Get started today! (sponsor)

The post Only 46% of Americans Have a Three-Month Emergency Fund. The Trend Is Getting Worse. appeared first on 24/7 Wall St..

You May Also Like

LIST: Bayanihan initiatives amid soaring oil prices

ASICID Launches Plug-and-Play Crypto Miners With Up to $25,590 Monthly Revenue

Report reveals what started Trump's feud with Italian pal: 'She doesn't see this as petty'

Trending News

More24/7 Live News

MoreQuick Reads

More