Must Read

After Ramon Monzon's nearly nine years as head of the local bourse, investors are entitled to ask whether the PSE's problems are merely structural or whether leadershipAfter Ramon Monzon's nearly nine years as head of the local bourse, investors are entitled to ask whether the PSE's problems are merely structural or whether leadership

[Vantage Point] PSE’s Monzon years: Rearranging the plumbing while the house burns

For feedback or concerns regarding this content, please contact us at crypto.news@mexc.com

The Philippine Stock Exchange has been passing reform after reform for almost a decade, but the market remains one of the region’s weakest performers. The harder question, however, remains unanswered: are new products the solution, or are they merely distractions from deeper problems of confidence, participation, and market relevance?

The Philippine Stock Exchange (PSE) has unveiled a reform package which aims to cure the country’s exchange-traded fund (ETF) framework by lowering capital requirements, allowing actively managed ETFs, broadening participation, and making it simpler for investment companies to bring products to market.

Does it sound modern? Does it sound like the kind of innovation a struggling stock market should embrace? The trouble is, this is the same story local and foreign investors have repeatedly heard over and over after nearly a decade under Ramon Monzon’s leadership.

From time to time, there’ll be some sort of reprieve. On Monday, global stocks rallied as oil prices eased. The PSE’s 300-point surge will no doubt be celebrated by bulls. The gains, however, were driven not by reforms from the PSE Tower, but by events unfolding in Washington and Tehran. The stock uptick follows news of a potential US-Iran peace breakthrough.

There’s no doubt that easing geopolitical tensions was what boosted risk appetite, but a stock exchange is ultimately judged not by a single day’s rally, but by how it performs against its peers over time — a far less flattering measure of the Monzon era.

Futile reforms

Every few years, another reform comes along. New products. New rules. New consultations. New frameworks. New roadmaps. Still, the scoreboard remains stubbornly unchanged.

The PSE remains dogged by chronic illiquidity, shrinking relevance, declining foreign participation, and a listing pipeline that would be considered anemic anywhere else in Southeast Asia.

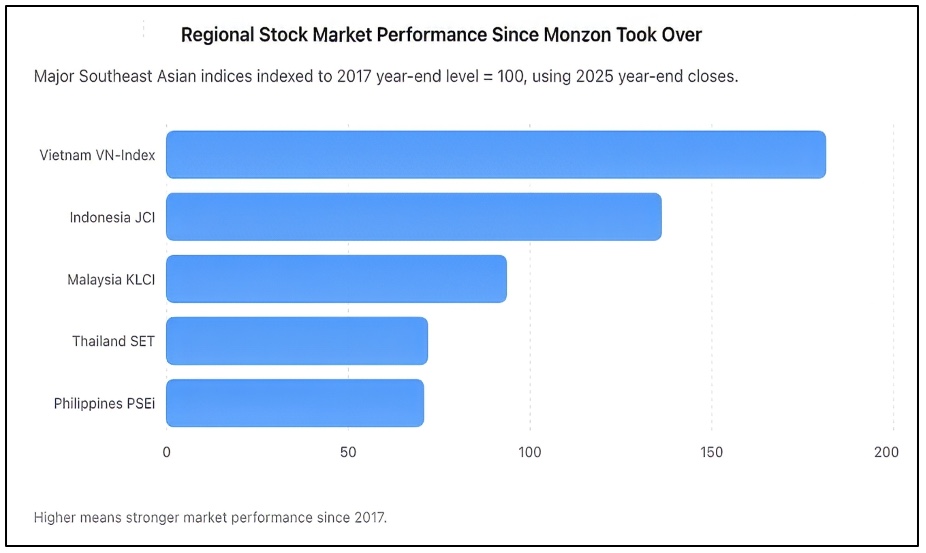

As shown above, from 2017 to 2025, the PSEi fell to 70.7 on an indexed basis, almost the same weak outcome as Thailand, while Vietnam nearly doubled and Indonesia rose strongly. The PSEi closed 2025 at 6,052.92, while Indonesia’s JCI closed at 8,646.94, Vietnam’s VN-Index at 1,784.49, Thailand’s SET at 1,259.67, and Malaysia’s KLCI at 1,680.11.

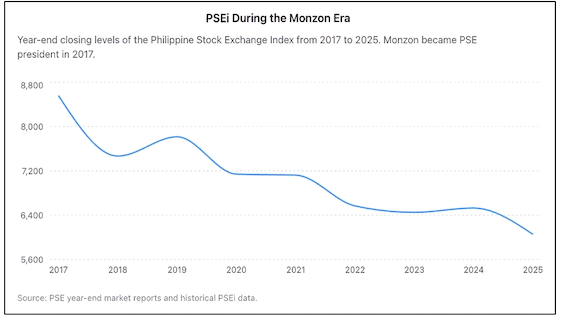

At some point, investors must stop being satisfied with promises and start looking at what they should get. There was plenty of optimism when Monzon stepped into leadership of the PSE in 2017. The benchmark index had just breached 8,500. The Philippines was being marketed as one of Asia’s emerging growth stories. Demographics, consumption, and remittances were growing, and corporate earnings were expanding. The expectation was that with the economy, the stock market would naturally deepen. Instead, the opposite happened.

PSEi struggles

Almost a decade later, the PSE Index remains well below its former highs despite years of economic growth. While new neighboring markets have attracted capital and drawn investors, the Philippines has steadily lost ground.

Nearly a decade of reforms, yet the Philippine stock market ended 2025 almost 30% below where it stood when Ramon Monzon took over the exchange, as shown in the chart above.

Bloomberg previously described the Philippine market as the worst-performing major stock market over the preceding decade, a humiliating distinction for a country that spent years promoting itself as one of Asia’s most promising investment destinations. Global conditions do not account for all of the deterioration. Every market faced the pandemic. Each market faced inflation, geopolitical shocks, and higher interest rates. But many recovered more quickly and emerged stronger. The Philippines did not. The evidence is visible everywhere.

Foreign investors have become consistent net sellers. Daily trading is minimal and tied closely to a small number of blue-chip stocks. Many listed firms trade only sporadically. Several companies have opted fully to delist, realizing that the price of remaining public is simply higher than the payoff. Only two companies completed initial public offerings in 2025. But that is not just disappointing for a nation of more than 110 million people. It is an indictment of the market’s inability to bring in new issuers.

Monzon’s supporters point to a series of new reforms imposed during his tenure. To be fair, there are many. The exchange pursued the acquisition of the fixed-income platform Product Disclosure Statement (PDS). It promoted Real Estate Investment Trusts (REITs). It pushed sustainability reporting. It modernized trading infrastructure. It advocated securities lending and borrowing. It supported short-selling. It encouraged digital participation and retail investing.

The issue is that reforms should be measured by results, not statements. A stock exchange has two fundamental functions. First, it needs to enable companies to effectively raise capital. Second, it must assist investors in deploying capital with confidence. On both measures, the PSE continues to struggle.

Is ETF the answer?

This is where the ETF initiative comes in. By significantly lowering capital requirements, allowing actively managed ETFs, and expanding the types of institutions that can launch products, the exchange aims to make ETF creation simpler.

That’s not a conceptual mistake, really. Mature markets across the globe experience thriving ETF industries because ETFs provide diversification, reduced costs, and greater accessibility. Yet ETFs don’t replace a healthy stock market. ETFs tend to do well in fact because lively capital markets already exist. It is not the reason that those markets became vibrant in the first place.

The United States didn’t become the world’s deepest capital market because it had ETFs. It made these ETFs because it already had thousands of listed companies, enormous institutional participation, deep liquidity, and strong investor confidence. The same can be said for markets such as Japan, Singapore, Australia, and Hong Kong.

The Philippines faces a far more fundamental challenge. Investors are not avoiding Philippine equities because there are too few ETFs. They are avoiding Philippine equities because they are questioning valuations, liquidity, governance standards, market depth, and long-term confidence.

Launching more ETFs in a market with limited liquidity risks simply redistributing existing money among the same small pool of securities. In other words, ETFs may improve the plumbing, but they do not fix the foundation.

The harder questions remain unanswered. Why does the Philippines continue to produce so few Initial Public Offerings (IPOs) relative to its economic size? Why do foreign investors remain persistent sellers? Why does market liquidity remain heavily concentrated in a handful of stocks? Why has the exchange failed to cultivate a robust pipeline of mid-sized growth companies? Why do many entrepreneurs still prefer private capital over public markets?

These are the questions that determine whether a stock exchange succeeds or fails. The uncomfortable reality is that confidence — not product innovation — is the market’s scarcest commodity. Ironically, Monzon himself has acknowledged that confidence is the most important ingredient in any capital market. On that point, he is absolutely correct.

But confidence cannot be legislated through circulars. It cannot be manufactured through new products. It cannot be restored through press releases announcing another reform package. Confidence is earned through competent performance.

Governance accountability

After nearly nine years, investors are entitled to ask whether the PSE’s problems are merely structural or whether leadership must also bear responsibility. A chief executive cannot take credit for every initiative while assigning every disappointing outcome to external factors. Leadership ultimately means accountability for results.

And so the ETF proposal, rational as it is in itself, should not be considered a turning point. It is an incremental improvement, not a revolution. It may make the market a little more efficient, but it’s not going to address the deeper problems the exchange has been grappling with for some time.

The challenge facing the PSE is not the lack of ETFs. Trust, liquidity, participation, and growth are absent here. But until those issues are addressed, any new reforms will likely be viewed less as an advance and more as an attempt to change the layout of the plumbing yet again, even as the house keeps losing residents because of a rickety foundation. – Rappler.com

Vantage Point Research Note: The above charts were prepared by Vantage Point from publicly available exchange data and year-end market reports. The analysis measures the performance of the Philippine Stock Exchange during Ramon Monzon’s tenure as president and Chief Executive Officer against regional peers using a common 2017 baseline. Sources include official PSE reports, historical PSEi records, and regional benchmark index data.

Click here for other Vantage Point articles.

Market Opportunity

Housecoin Price(HOUSE)

$0.0014901

$0.0014901$0.0014901

USD

Housecoin (HOUSE) Live Price Chart

Disclaimer: The articles reposted on this site are sourced from public platforms and are provided for informational purposes only. They do not necessarily reflect the views of MEXC. All rights remain with the original authors. If you believe any content infringes on third-party rights, please contact crypto.news@mexc.com for removal. MEXC makes no guarantees regarding the accuracy, completeness, or timeliness of the content and is not responsible for any actions taken based on the information provided. The content does not constitute financial, legal, or other professional advice, nor should it be considered a recommendation or endorsement by MEXC.

You May Also Like

Ethereum Price Outlook Clouds as Top Foundation Executive Steps Down

Key Insights: Ethereum (ETH) price had already been soft in mid-June, sliding from above $2,000 to around $1,700. Then the Ethereum Foundation added another layer

Share

Thecoinrepublic2026/06/20 08:00

GBTC’s 1.50% Fee Is Subtly Costing You Thousands Every Decade

If you own Grayscale Bitcoin Trust (NYSE:GBTC), you are paying a premium for Bitcoin exposure that nearly identical funds now sell for a fraction of the price.

Share

247 Wall St.2026/06/20 08:16

EEM’s 0.69% Fee Quietly Costs You $690 a Year, but Your Cheaper Alternative Charges $90

If you hold iShares MSCI Emerging Markets ETF (NYSEARCA:EEM), BlackRock skims 0.69% of your account every year before you see a single dividend. That is roughly

Share

247 Wall St.2026/06/20 08:42