RLUSD vs USDC: Can AI-Agent Payments Give Ripple a Real Stablecoin Use Case?

At 2:07 a.m., a warehouse robot flags a failing sensor and purchases a replacement part on its own. The order clears in seconds as the bot’s agent chooses a stablecoin rail with guaranteed settlement and a per-transaction budget. Was that USDC or Ripple’s RLUSD under the hood?

That question suddenly matters. On June 10, 2026, Mastercard unveiled “Agent Pay for Machines,” a service built to let AI agents transact at machine speed with guaranteed settlement across cards, bank accounts, and stablecoins, with 30+ launch partners including RippleX, Coinbase, OKX, Aave Labs, Solana Foundation, and Polygon (Mastercard press release (PDF)).

Just a week earlier, Mastercard said it will expand on-chain/card settlement to include six regulated stablecoins at launch — USDC, PYUSD, USDG, USDP, RLUSD, and SoFiUSD — and enable settlement across Ethereum, Solana, Polygon, Base, Arbitrum, Canton, Tempo, and the XRP Ledger (Mastercard press release).

Stablecoins are moving from crypto-native rails into mainstream settlement networks and, now, into autonomous agent workflows. USDC retains a dominant footprint, with Circle reporting $74.8 billion in circulation as of June 11, 2026 (Circle). Ripple, meanwhile, is positioning RLUSD to play in regulated corridors and enterprise-facing integrations: RLUSD’s on-chain market value hovered around $1.6–$1.8 billion in early June, and Ripple announced new Turkish institutional access via BiLira, Bitexen, and Bitlo (Ripple press release / CoinDesk coverage).

Merchants, marketplaces, IoT manufacturers, and treasury teams are the immediate stakeholders. The near-term contest is not a meme-driven flippening; it’s a routing game about which coin reliably clears across banks, cards, and chains with the fewest operational surprises.

RLUSD and USDC at a glance in 2026

USDC and RLUSD both sit inside Mastercard’s expanding settlement framework, but they start from very different bases. Here is a high-level view:

Category USDC RLUSD Circulation (June 2026) $74.8B reported by Circle on Jun 11, 2026 (Circle) ~$1.6–$1.8B cited in early June (Ripple / CoinDesk) Issuer Circle Internet Financial Ripple (Ripple USD) Settlement scope announced Included in Mastercard’s six-stablecoin expansion across multiple blockchains (Mastercard) Included in the same Mastercard expansion, with XRP Ledger named among supported networks (Mastercard) AI-agent readiness Part of Mastercard’s Agent Pay partner set via the broader settlement program (Mastercard) RippleX listed among Agent Pay’s initial partners, signaling integration pathways for RLUSD (Mastercard) Ecosystem depth Broad integrations across exchanges, custodians, and fintechs Growing institutional corridors; smaller market cap but expanding partnerships (e.g., Türkiye)

Scale is the headline difference: USDC’s float gives it liquidity and pricing advantages in most venues. RLUSD’s angle is targeted corridors, enterprise integrations, and now potential access to card/bank rails through Mastercard’s programs.

How AI-agent payments change stablecoin utility

AI-agent payments compress the decision window for settlement — a machine chooses a rail in milliseconds and must adhere to policy. Mastercard’s “Agent Pay for Machines” is designed for that reality, offering programmable budgets and guaranteed settlement across fiat and on-chain options, with 30+ partners at launch including RippleX, Coinbase, and OKX (Mastercard).

What an agent actually does at checkout

- Check policy: verify budget, merchant category, geography, and compliance rules.

- Quote rails: fetch settlement quotes across card, bank transfer, and supported stablecoins.

- Select route: choose the rail with the best mix of cost, latency, and acceptance probability.

- Execute and lock: initiate payment with guaranteed settlement parameters.

- Reconcile: write receipts on-chain or to enterprise ledgers for audit and inventory.

Guaranteed settlement and programmable limits

For agents, “guaranteed settlement” can beat raw speed. A slightly slower rail that guarantees finality and refundability may be preferable to a faster, probabilistic one. Programmed limits ensure a runaway agent cannot drain treasuries — crucial for industrial IoT and API-driven commerce.

Routing neutrality favors coins with reach

In an agent world, brand recognition fades. What matters is where the coin can actually clear with minimal slippage and operational frictions. That’s an advantage for USDC today, but RLUSD’s alignment with enterprise corridors and card/bank infrastructure could reduce that gap in specific flows.

Rails and reach: where each coin can actually settle

On June 3, Mastercard said it will support six regulated stablecoins — including USDC and RLUSD — for settlement across a mix of public and permissioned chains: Ethereum, Solana, Polygon, Base, Arbitrum, Canton, Tempo, and the XRP Ledger (Mastercard). That matters for two reasons:

Card and bank interoperability

If a merchant’s acquirer can settle in stablecoins, and an agent can trigger a card-like authorization with stablecoin finality underneath, the merchant’s operational model simplifies. The merchant can standardize reconciliation through their acquirer while still benefiting from on-chain programmability.

On-chain settlement domains

Settlement support on multiple networks creates a larger, more resilient clearing surface. USDC historically maintains a multi-chain footprint and deep exchange support, which translates to broad acceptance. RLUSD’s inclusion alongside USDC in Mastercard’s expansion suggests enterprises could access RLUSD via familiar payment interfaces while still benefiting from XRP Ledger settlement where appropriate — especially relevant for corridors where Ripple has relationships.

In short: USDC brings network effects; RLUSD brings corridor specificity and enterprise-friendly integration pathways. AI-agent routing engines will arbitrage both.

Regional expansion vs network effects

Ripple’s June 2 announcement spotlighted Türkiye, where RLUSD is now available to institutions via BiLira, Bitexen, and Bitlo partnerships, with on-chain market value around $1.7 billion at the time (Ripple press release / CoinDesk coverage). That move aligns with Ripple’s long-standing focus on cross-border and bank/fintech integrations.

Why Türkiye matters

Türkiye sits at an active crossroads for remittances and SME trade. Institutional access creates the conditions for corporate treasurers and fintechs to pilot RLUSD in real corridors: supplier prepayments, marketplace disbursements, and PSP-to-PSP settlement.

USDC’s counter-position

USDC’s sheer scale — $74.8B in circulation as of June 11 — and its long-standing integrations with exchanges, custodians, and fintechs provide liquidity depth and price discovery (Circle). For most global marketplaces, that liquidity can outweigh the benefits of a more targeted corridor, unless the corridor unlocks materially lower costs or regulatory clarity.

How AI agents might choose

If a Turkish marketplace offers better incentives or acceptance probability on RLUSD — especially when paired with an acquirer or PSP integrated into Mastercard’s stablecoin settlement — agents could favor RLUSD for local flows while defaulting to USDC for international orders. The result could be a stablecoin mix optimized by geography, acceptance, and merchant policy.

What this means for builders and treasurers

Agent-driven payments force more disciplined settlement design. Whether you are a marketplace PM, an IoT OEM, or a treasury lead, focus on rails, rules, and reconciliation — not coin tribalism.

Practical steps to evaluate USDC vs RLUSD in your stack

- Map acceptance and corridors: list your top settlement geographies and PSP/acquirer partners; verify which support USDC, RLUSD, or both under Mastercard’s programs.

- Define agent policy: set per-agent budgets, MCC whitelists, and approved rails; ensure fallbacks between card, bank, and stablecoin routes.

- Test latency and failure modes: run side-by-side agent simulations for USDC and RLUSD across typical order sizes and peak times; log declines, reversals, and retry success rates.

- Model liquidity buffers: size working capital in each coin to meet daily agent demand without incurring repetitive FX or bridge costs; include stress scenarios.

- Close the books: standardize receipts and sub-ledgers; ensure audit trails from the chosen settlement network to your ERP.

When RLUSD could be the right tool

If your flows align with Ripple’s institutional corridors (e.g., Turkish partners) or if a PSP offers better pricing/acceptance on RLUSD through Mastercard’s framework, RLUSD may deliver superior net economics for those routes. The smaller float can be a feature if it comes with closer issuer support in a given corridor.

When USDC likely wins

For broad, multi-market commerce and DeFi-adjacent liquidity needs, USDC’s circulation and integrations make it a default choice. Agents benefit from high acceptance probability and thicker order books for on/off-ramping — particularly useful for global marketplaces and high-volume API commerce.

Risks & What Could Go Wrong

- Regulatory swing risk: issuer or corridor-specific rulings can constrain where and how a stablecoin can settle.

- Depeg and liquidity gaps: stress events can widen spreads or break par temporarily, impacting agent routing and merchant pricing.

- Smart-contract or network outages: chain congestion or incidents can stall on-chain finality even if card authorizations succeed.

- Counterparty and custodial exposure: settlement assurances are only as strong as issuer backing and program agreements.

- Agent misconfiguration: poorly set budgets or policy rules can trigger unauthorized or cascading transactions.

- Compliance friction: KYC/AML and travel-rule requirements vary by corridor; mismatches can lead to declines or funds held for review.

If you track these developments daily, outlets like Crypto Daily curate ongoing changes across issuers, PSPs, and settlement networks so builders can adjust roadmaps without chasing headlines.

Frequently Asked Questions

What is RLUSD and how does it differ from USDC?

RLUSD is Ripple’s U.S. dollar stablecoin. USDC is issued by Circle. Both are designed to hold a $1 peg, but they differ in circulation scale, ecosystem integrations, and corridor focus. As of mid-June 2026, USDC’s supply is about $74.8B (Circle), while RLUSD’s on-chain market value was roughly $1.6–$1.8B in early June (Ripple / CoinDesk).

How does Mastercard’s Agent Pay affect stablecoin adoption?

Agent Pay creates a standardized way for AI agents to transact with guaranteed settlement across cards, bank accounts, and supported stablecoins, listed with 30+ partners including RippleX. It prioritizes routing reliability and policy controls over brand visibility (Mastercard).

Will merchants be able to settle in RLUSD and USDC through Mastercard?

Mastercard announced plans to expand settlement to six regulated stablecoins, including USDC and RLUSD, across multiple networks. Merchant availability depends on acquirers/PSPs and regional readiness, so timelines can vary by partner and jurisdiction (Mastercard).

Does RLUSD’s Türkiye push change the calculus for AI-agent payments?

It can in that corridor. If Turkish institutions and PSPs support RLUSD directly and offer favorable terms, agent routing engines may prefer RLUSD for domestic or regional flows while retaining USDC for cross-border scenarios (Ripple press release / CoinDesk coverage).

Which is better for DeFi liquidity today — USDC or RLUSD?

USDC generally enjoys deeper liquidity and broader integrations across exchanges and DeFi venues, which can improve pricing and slippage. RLUSD’s strengths today appear more corridor- and enterprise-focused, though this could evolve as integrations expand.

Do I need to adopt the XRP Ledger to use RLUSD with agents?

Not necessarily. Mastercard’s settlement framework aims to abstract rails for merchants and agents, and it lists multiple chains — including the XRP Ledger — for stablecoin settlement. Actual integration paths will depend on your PSP/acquirer and issuer connectivity.

How should treasuries manage multi-coin exposure with agents?

Set policy-driven buffers per rail, monitor spreads and settlement SLAs, and maintain contingency routes. Treat each coin and settlement path as a separate vendor risk with clear escalation and rollback procedures.

Disclaimer: This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.

You May Also Like

DC insider shoots down 'desperate' JD Vance's presidential dreams: 'No natural skills'

Cancer patient among 100,000 red state voters who lost food aid under Trump's new law

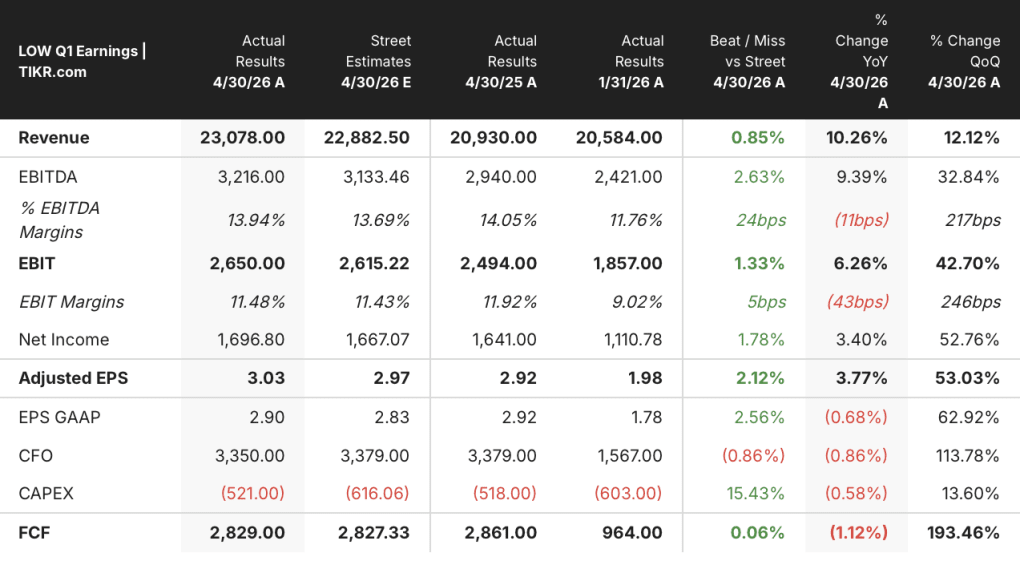

Why Lowe’s Stock Looks Undervalued After Its Q1 Margin Compression Results in 2026