Recently, U.S. President Donald Trump signed an executive order that, for the first time, authorizes 401(k) retirement savings plans to include digital assets, such as bitcoin, ether, and other cryptocurrencies, within their investment portfolios. This landmark policy directly links the United States’ largest retirement fund pool, valued at approximately $9 trillion and covering more than 90 million participants, to the cryptocurrency market. This article provides a comprehensive analysis of the potential structural changes and long-term implications of this development, examining the framework of the 401(k) system, the policy change background, estimated capital inflows, implementation pathways, and the broader market impact.

A 401(k) plan is a long-term retirement savings program established by U.S. employers for their employees. It enables employees to allocate a portion of their pre-tax salary into an investment account, benefiting from tax deferral. The primary objective is to help employees accumulate sufficient savings over time to achieve financial security in retirement. Participants generally select from an employer-curated investment menu, typically comprising mutual funds across various asset classes. Employers frequently offer matching contributions as part of their benefits packages, further incentivizing participation. As one of the most prevalent retirement savings vehicles in the United States, the 401(k) covers tens of millions of workers and manages assets worth trillions of dollars.

Key features include:

Tax Deferral: Contributions are made from pre-tax income, with taxes deferred until withdrawals in retirement.

Employer Matching: Employers often contribute an additional amount based on a percentage of the employee’s contributions.

Defined Investment Options: Portfolios typically consist of 20–30 funds selected by the employer, spanning equities, fixed income, and certain alternative assets.

Fiduciary Obligation: Employers must adhere to the prudent-person rule to ensure investment options are appropriate in terms of risk, or face potential legal liability.

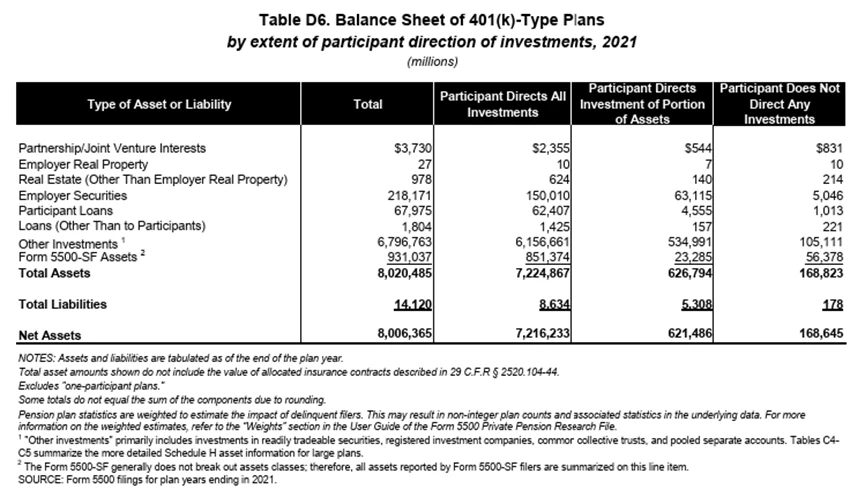

According to the U.S. Department of Labor, total 401(k) assets were approximately $8 trillion in 2021. The Investment Company Institute reports that this figure had risen to $8.7 trillion by the first quarter of 2025. The White House further disclosed that over 90 million Americans are currently enrolled in the program.

Traditionally, the investment menu for 401(k) plans is curated by employers and typically includes 20–30 stock, bond, and select alternative funds. These investment products are required to be safe and stable, subject to the prudent-person rule to ensure appropriate risk protection for participants.

In 2020, the U.S. Department of Labor made an initial attempt to introduce private equity assets into 401(k) plans. However, the initiative achieved little traction due to limited liquidity and regulatory misalignment. The current policy represents a significant departure from that effort, marked by stronger top-level policy backing and more robust multi-agency regulatory coordination. Its most notable breakthrough is the removal of the longstanding barrier to digital assets, allowing for the first time mainstream cryptocurrencies such as Bitcoin and Ethereum, together with related compliant financial products, to be included as eligible 401(k) investment options.

In contrast to the Department of Labor’s past, loosely defined guidance limited to private equity, this presidential executive order demonstrates far greater policy force. It involves coordinated participation from multiple agencies, including the U.S. Department of the Treasury, the Securities and Exchange Commission (SEC), and the Department of Labor, significantly enhancing the policy’s systemic reach and regulatory rigor.

While the policy opens the door for digital assets in retirement plans, actual capital inflows will still face several procedural hurdles. Under the current regulatory framework, implementation is expected to proceed in three phases:

Department of Labor Rulemaking: Define limits on cryptocurrency investment allocations, eligible product types, and disclosure requirements.

Financial Institution Product Development: Asset managers design compliant crypto asset funds, prioritizing SEC-approved spot ETFs.

Employer Menu Updates: Employers evaluate and determine whether to add new funds to their investment lists, after which employees can choose their allocation.

The full rollout is projected to take 6 to 24 months.

The 401(k) system manages an enormous pool of assets, currently approaching $9 trillion. Assuming just 2% of these funds are allocated to digital assets, approximately $170 billion in long-term capital could flow into the cryptocurrency market. This amount is equivalent to about 65% of the total global crypto spot ETF and institutional holdings (roughly $260 billion), enough to have a significant impact on the market structure.

The entry of long-term capital could improve the funding composition of the crypto market, reduce short-term speculative volatility, and enhance market liquidity and price stability. Moreover, the steady investment style of pension funds could foster a gradual “slow bull” trend, accelerating the institutionalization and mainstream adoption of crypto assets. This shift could not only boost market confidence in digital assets but also attract more traditional investors to participate.

The first crypto assets likely to appear in 401(k) menus are crypto spot ETFs, regulated by the U.S. Securities and Exchange Commission (SEC) for strong compliance, secure custody, transparent valuation, and high liquidity, making them well-suited for pension investment. These ETFs will likely be included in Target Date Funds (TDFs) or balanced funds. While allocations may be small, their market impact could be significant and lasting.

As crypto enters 401(k) plans, both investors and fund managers must prioritize risk control and prudent allocation. Most guidance suggests limiting crypto exposure to no more than 5% of the portfolio, focusing on products with high compliance and liquidity, transparent valuation, and secure custody.

Investors should align leverage and position sizes with their risk tolerance and investment horizon, reducing the effect of short-term volatility on long-term savings. Employers, as fiduciaries, must follow the prudent-person rule, rigorously assessing product compliance and risk. Ultimately, disciplined risk management and careful asset selection will be key to safely integrating digital assets into 401(k) plans, allowing pension funds to diversify and grow while preserving stability.

President Trump’s executive order marks the beginning of a new era in which the U.S. retirement savings system and the cryptocurrency market enter into deep integration. While actual capital inflows will take time, the scale of this long-term capital could drive structural optimization and institutionalization within the crypto market, becoming a key engine for sustainable growth. With bitcoin, ether, and other core digital assets formally included in 401(k) plans, the entry of long-term funds is set to significantly reshape the market landscape. This transformation brings unprecedented opportunities but also challenges, particularly in the form of market volatility and regulatory uncertainty. Effective risk management and disciplined asset allocation will be critical to protecting investor interests and achieving steady capital appreciation.

As the regulatory framework matures and market mechanisms improve, pension fund allocations to core digital assets will help promote industry standardization and sustainable development, injecting new vitality and confidence into the digital economy. Investors should closely monitor policy developments, uphold fiduciary responsibilities, and actively build compliant, resilient investment systems, fostering deeper integration and innovation between digital assets and traditional finance.

Recommended Reading:

Why Choose MEXC Futures?Discover the unique advantages of trading Futures on MEXC and learn how to stay ahead in the derivatives market. How to Participate in M-Day?Master the steps and strategies for joining M-Day events and don’t miss out on daily airdrops of over 70,000 USDT in Futures bonus rewards.

MEXC has officially rolled out its0-Fee Festevent, empowering users to significantly reduce their trading costs. With this initiative, users can truly save more, trade more, and earn more. By participating in the campaign, you'll enjoy ultra-low-fee trading on the MEXC platform while staying ahead of market trends and seizing fleeting investment opportunities the moment they arise. It's your gateway to smarter trading and greater wealth growth.

Disclaimer: The information provided in this material does not constitute advice on investment, taxation, legal, financial, accounting, or any other related services, nor does it serve as a recommendation to purchase, sell, or hold any assets. MEXC Learn offers this information for reference purposes only and does not provide investment advice. Please ensure you fully understand the risks involved and exercise caution when investing. MEXC is not responsible for users' investment decisions.